Keep these questions in mind as you plan your next college visits and take the time to schedule an appointment with the school’s office of financial aid.

1. What are your financial aid deadlines?

In addition to deadlines for the standard financial aid applications: the Free Application for Federal Financial Aid (FAFSA) and PROFILE, the financial aid application service of the College Board, colleges may also have their own deadlines and forms. Be sure to ask if the school’s financial aid forms are different for need-based and merit-based aid when the deadlines are. Note many schools have declared March 1 as their priority filing date for financial aid. Be sure to confirm each school’s priority filing dates.

2. What is your Cost of Attendance (COA) for the current year?

There are precisely six components to a college student’s complete budget:

- Tuition

- Fees

- Room and Board

- College Textbooks and Supplies

- Personal expenses

- Transportation

Many proposed budgets only include Direct Costs (which are the first three items listed) and typically what you will pay directly to the bursar’s office. However, the U. S. Department of Education requires that colleges fully inform you as to all of the above costs, so find out specifically what those amounts are to establish a complete budget for college expenses.

3. How much of an increase in the COA do you project for next year?

When you ask this question, be sure to request the specifics related to each cost component. Tuition and Room and Board increases are independent of each other. For example, one school may expect an increase of 5 percent in tuition and fees, but a 10 percent increase in Room and Board. This information will help with budgeting but also gives the financial aid officer the impression that you are an informed parent.

4. Are you able to meet 100 percent of financial need?

If they say “No,” find out why, and get details. Is the policy based on “first come, first served?” What’s the average percentage of need the school can meet? What percentage is in the form of grants and how much is in the form of loans? Is there a dollar amount left as a gap (unmet need) for everyone? Do they include Parent Loans (PLUS) in the aid package?

(Note: They shouldn’t do this…those loans are to be used for your EFC-Expected Family Contribution, not for meeting the financial need of the student.)

5. Do you offer Merit Scholarships, and how do you treat private scholarships awarded to the student?

If a Merit Scholarship is being awarded, it normally goes into the financial aid package first, reducing the amount of need-based aid. Find out if a merit award reduces the self-help in the package, or if it replaces other need-based grants. A true Merit Scholarship can go beyond the “need” level, which means that it can lower your EFC.

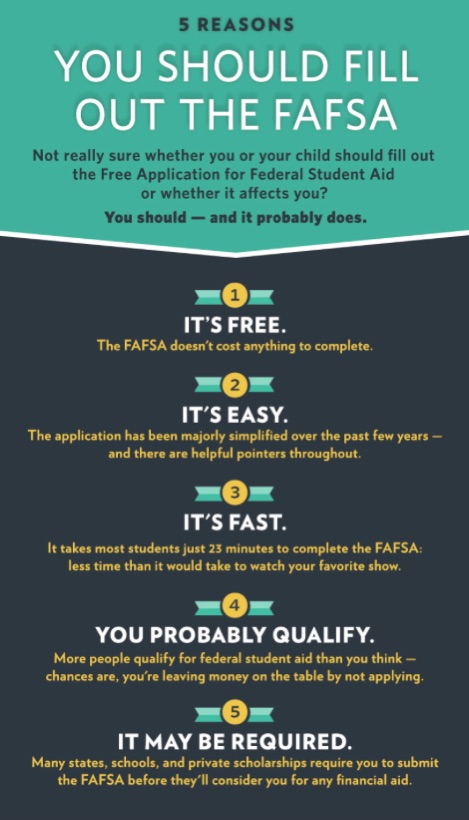

It’s FAFSA time. “Yuck”, as one parent said. “Dreading, dreading, dreading” from another. “It’s my least favorite time of year (other than income taxes)”, said another. I get it. Nobody likes filling out federal forms, especially when money is on the line. And with the FAFSA, money is on the line.

It’s FAFSA time. “Yuck”, as one parent said. “Dreading, dreading, dreading” from another. “It’s my least favorite time of year (other than income taxes)”, said another. I get it. Nobody likes filling out federal forms, especially when money is on the line. And with the FAFSA, money is on the line.