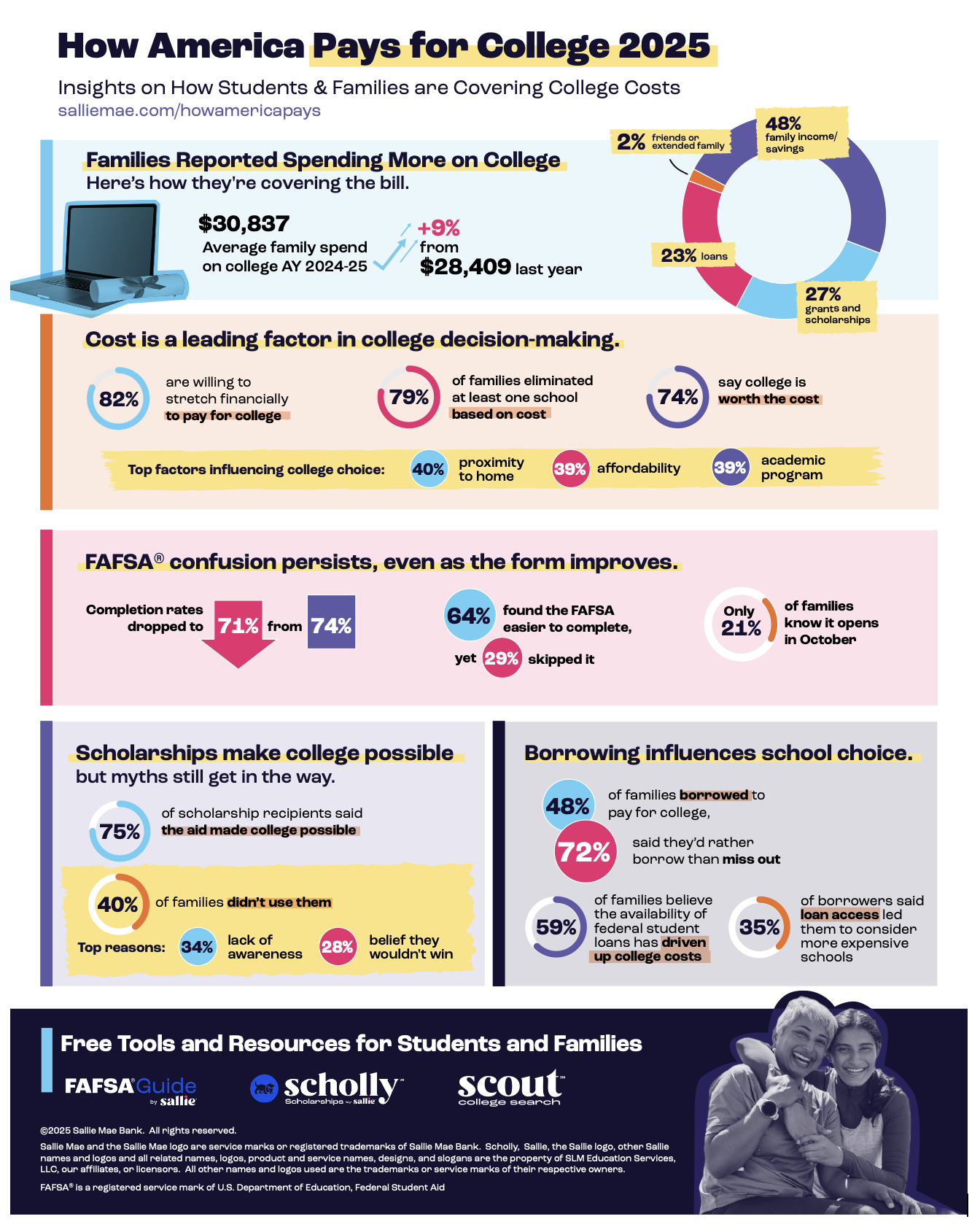

Families reported spending an average of $30,837 on college during the 2024–25 academic year—up 9% from $28,409 last year and a return to pre-pandemic spending levels, according to “How America Pays for College 2025,” the annual study by Sallie Mae and Ipsos. Family income and savings covered nearly half of costs (48%), followed by scholarships and grants (27%), borrowing (23%), and contributions from family or friends (2%).

For more detailed information beyond the graphic above, you can download the full report here.

A college education is one of the biggest investments you could ever make. College costs money, and it’s not often as cheap as you think it could be. The good news is that it doesn’t have to cost you everything you have, and you do not need to live on ramen the entire time you’re studying.

Your education is important, and you have to look at it as the investment that it is. If you’re planning on studying a useful degree, then you’re going to know that whatever you put into it now is going to pay you back later.

Low interest student loans are out there for those who want to use them, but you must also consider other ways to contribute toward affording college. You get to crunch the numbers now and plan for your future to make it as bright as possible.

Are you looking for ways to support your child’s academic journey without breaking the bank? Creating a scholarship strategy could be the answer! Encouraging your students to apply for scholarships can not only alleviate financial burdens but also open doors to incredible opportunities.

Here are some tips to help guide your child through the scholarship application process:

With consumer finances facing further turbulence following the announcement of the August resumption of U.S. student loan repayment, young Americans are bracing themselves for a financial squeeze in advance of the holidays.

With evidence that shoppers are already showing caution – the savings experts at SimplyCodes have put together some practical money advice for young consumers on how to navigate an increasingly compressed disposable income and how to better manage student loan repayments being back on the list of monthly expenses.

If you’re a parent of a college-bound teen, you know the stress this adds to your family. If you are like most parents, the money you saved for college has not kept up with the increase in tuition. If your son or daughter isn’t one of the ones who snag a full ride, you are going to be looking for ways to cut those college costs.

Here are just a few tips that might help you pay less for college:

I will never forget the moment we received our Student Aid Report and I saw the EFC (Expected Family Contribution) on the right-hand corner. I was in shock as most parents are. How could the powers that be believe we could afford to pay that amount for college? It was a mystery to me how they came up with that number, as it is to most of you.

The EFC determines how much financial aid the colleges will award to your student. You can’t receive any federal or institutional aid without getting an EFC when you complete the FAFSA. We are stuck with it and will probably never truly understand how they use to determine how much money your family can afford to pay.

If you are going to need financial aid for college (and who doesn’t?), you will need to understand the EFC.

Debt from college tuition has skyrocketed over the last several years. Parents and students are weighing their ROI (return on investment) before making their college choices. As college costs have shot up, so has student debt. How can you pay for college without incurring debt?

According to the latest Quarterly Report on Household Debt and Credit, outstanding student loan debt stood at $1.58 trillion in the fourth quarter of 2021, an $8 billion decline from the third quarter. About 5 percent of aggregate student debt was 90+ days delinquent or in default in the fourth quarter; the lower level of student debt delinquency reflects a Department of Education decision to report current status on loans eligible for CARES Act forbearances.

That’s the bad news. But if you’re a savvy consumer and research the costs before signing on the dotted line, you should be able to go to college without incurring debt. Zac Bissonnette, author of DebtFree U, is proof that it can be done. He graduated from college with zero debt.

Believe it or not, you may be able to graduate without debt if you use these 10 ways to pay for college:

Studies have shown that students who spent time working during college actually do better in the classroom. Students who work must learn how to structure and manage their time to work around class assignments. This translates into not delaying assignments and scheduling time to study for exams. However, many experts suggest that freshmen students wait until the second semester to take on the added responsibility of a job. This allows them time to ascertain their academic strengths and decide whether or not a job would detract from their study time.

When college students do decide to work, there are three options available to them: on-campus jobs, off-campus jobs and internships. Each of these job opportunities has its own set of advantages.

Many students neglect applying for scholarships with small awards. However, every small award your student receives means more free money to pay for college.

The RevenueZen Social Selling Scholarship is an award for any current or soon-to-be undergrad who is looking to innovate the hiring process. In an ideal world, what would hiring and applying for a job look like? How will you stand out? The RevenueZen Scholarship has a brief submission process, and applicants will be judged on their ability to convey their idea for an innovative social selling process focused on getting hired at a specific company.

In the wake of the coronavirus crisis, many American families are under severe financial strain and parents of college-bound students are in need of financial aid. Many are facing a $40,000 college tuition bill.

Nearly 40% of parents who didn’t plan to apply for federal aid, now will as a result of the pandemic, according to a recent survey by Discover Student Loans.

Roughly half of parents lost income as a result of the pandemic and 44% said they can’t afford to pay for as much of their child’s education as they had originally planned, the survey found.