Every year, parents suddenly start searching the term “529 plans”. Search interest tends to spike around tax season, policy announcements, or financial planning milestones, and that surge tells an important story.

Parents aren’t just curious. They’re actively looking for smart ways to save for college while navigating rising tuition, changing rules, and long-term family finances.

If you’ve recently found yourself wondering whether a 529 plan makes sense, or if you’re revisiting your savings strategy, you’re right on schedule. These spikes in attention often coincide with moments when families pause to reassess their financial priorities. The key is turning that moment of interest into informed action.

If you’ve found yourself Googling “Is college worth it?” or “college ROI vs student debt,” you’re not alone.

As 2026 approaches, more parents and students are asking important questions. As college costs keep rising, parents nationwide are searching for answers about college ROI, student loan debt, and whether a degree still offers long-term value. For families with college-bound teens, understanding the true cost of college, and what return you can realistically expect, has become one of the most crucial financial decisions parents will make.

Let’s honestly discuss what “return on investment” truly means when it comes to college and how parents can evaluate it without turning the process into a math problem that takes away the joy of this milestone.

There are a few tried and tested ways to transform your financial habits, but no one ever really thinks about how online learning can help. There are many advantages to learning online that help with money, including learning how to budget better, and greater freedom and flexibility.

Better Financial Literacy

You can use online courses to learn the basics of financial literacy with concepts like compound interest, inflation, and even risk management. When you have foundational knowledge like this, the rest kind of falls into place and becomes much clearer. As a result, you can make informed decisions based on data and experience instead of feeling. The College Investor and other sites like it also have tons of informative articles you can use to get a head start.

If you’re the parent of a college-bound teen, you’ve probably heard the same thing again and again: college costs are rising. Tuition goes up. Fees go up. Housing and meal plans? Also up. And if you’ve ever found yourself staring at those numbers, wondering how families are expected to keep up, you’re definitely not alone.

Tuition increases are changing the entire college-planning conversation for families. Understanding why it’s happening and what it means for your teen’s future can help you plan more confidently.

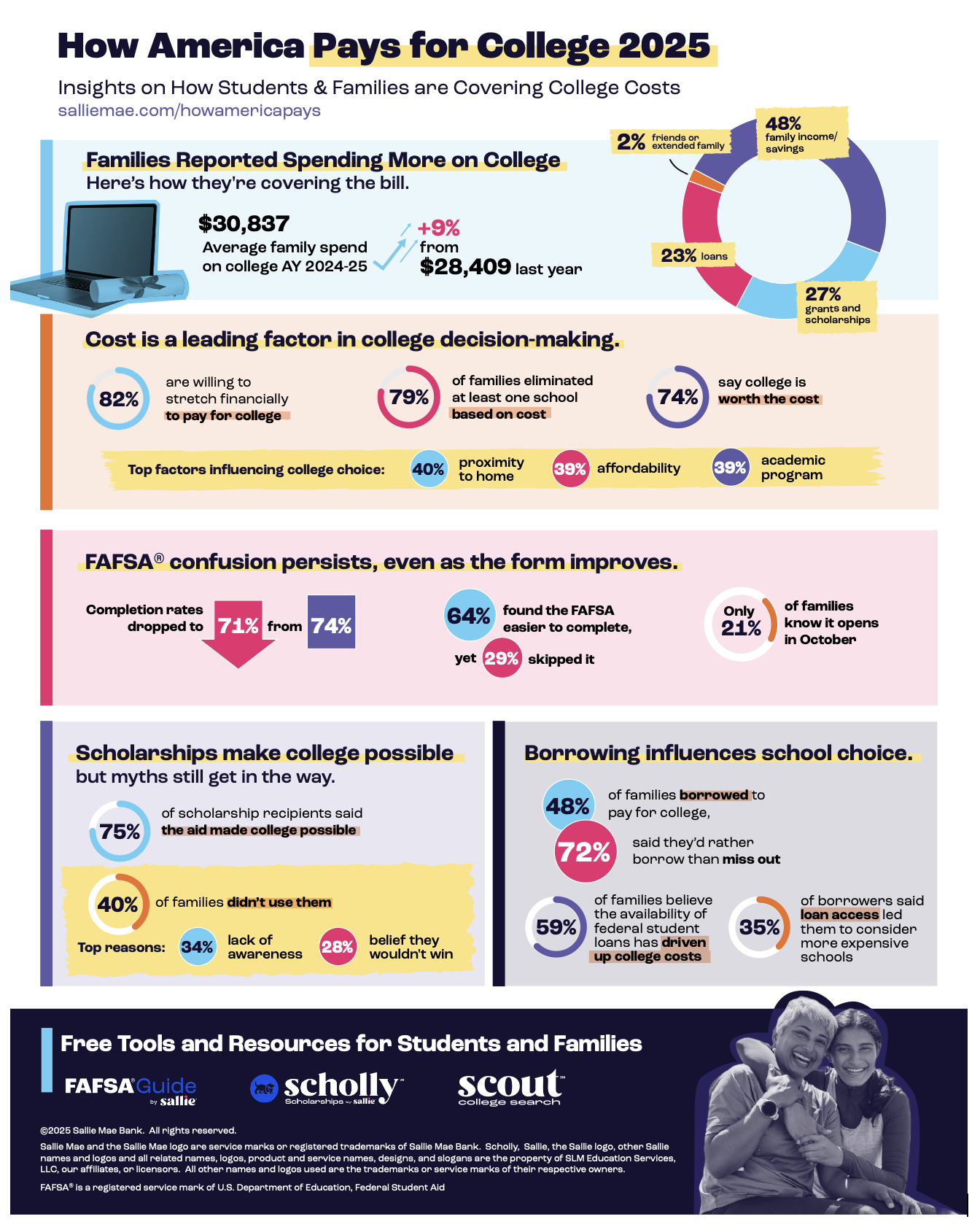

Families reported spending an average of $30,837 on college during the 2024–25 academic year—up 9% from $28,409 last year and a return to pre-pandemic spending levels, according to “How America Pays for College 2025,” the annual study by Sallie Mae and Ipsos. Family income and savings covered nearly half of costs (48%), followed by scholarships and grants (27%), borrowing (23%), and contributions from family or friends (2%).

For more detailed information beyond the graphic above, you can download the full report here.

For many families, even after financial aid, scholarships, and federal loans are applied, there’s still a gap between what college costs and what’s covered. That’s where private student loans can be a helpful solution. While they often get a bad reputation, private loans can be a valuable tool for parents who want to support their child’s education—especially when used thoughtfully and strategically.

The Benefits of Private Student Loans

Closing the Funding Gap: Private loans allow families to cover costs that federal loans and savings can’t. This ensures your child doesn’t have to compromise on the right school or program simply because of finances.

Potentially Lower Rates: Parents with strong credit can often qualify for competitive, even lower, interest rates compared to federal Parent PLUS loans. This can save significant money over the life of the loan.

Flexible Amounts: Unlike federal loans, which have borrowing limits, private loans often allow you to borrow enough to cover the full cost of attendance.

Fast Processing: Many private lenders offer quick approvals and disbursements, which can ease the stress of looming tuition deadlines.

Customizable Repayment Options: Some lenders offer a range of repayment plans, including options to make interest-only payments while your child is in school, helping keep balances manageable.

If you’re the parent of a college-bound student, you’ve probably had a few sleepless nights wondering: How are we going to afford this? Between rising tuition, student loan anxiety, and the pressure to launch into the workforce quickly, the traditional four-year degree may feel out of step with today’s realities.

Choosing a college is one of the biggest decisions your student will make, but as a parent, you play a crucial role in guiding them through the financial and logistical challenges that come with it. What happens when your child’s college plans don’t match your budget or comfort level? Let’s tackle some common concerns and explore ways to navigate these tough college decisions with your student.

Navigating the financial aid process can feel like wading through a maze of forms, deadlines, and unfamiliar terms. It can seem overwhelming for many parents, especially first-time or first-generation college families. But with a little guidance, you can make a significant difference in your student’s ability to afford college. Let’s break it down step by step to help you confidently tackle the process.

1. Know the Key Financial Aid Forms

The first step in applying for financial aid is understanding the forms you must complete. The most common ones include:

FAFSA (Free Application for Federal Student Aid): This is the gateway to federal grants, loans, and work-study opportunities. Many states and colleges also use FAFSA information to determine their aid packages.

CSS Profile: Some colleges, particularly private institutions, require this additional form to award institutional aid. It digs deeper into your family’s financial situation than the FAFSA.

Make sure to check the requirements for each college your child is applying to and note whether they require just the FAFSA, or both forms.

Starting college is exciting. It’s a chance to learn, meet new people, and prepare for your future. But along with the excitement comes a long list of costs. College can feel expensive fast. Luckily, by understanding the key expenses and planning ahead, you can handle them without too much stress. Here’s a breakdown of what to expect and how to manage the college costs.