If you have kids, then chances are you’ve already thought about college affordability and how or if you’ll be able meet the expenses associated with higher education.

If you have kids, then chances are you’ve already thought about college affordability and how or if you’ll be able meet the expenses associated with higher education.

But you shouldn’t allow the worry of college costs to consume your life. There are many practical and successful ways to pay for college (without drowning in debt) no matter what your income level may be.

Many families labor financially to make ends meet and they feel like it will be impossible for their children to attend a 4-year university. This simply isn’t the case. I’m not saying it’s going to be easy, but there are ways to send your children to college on just about any level of income.

Saving For College – Reduce Your Debt

Anyone can save money for college; all you need is to remove the excuses from your life. Starting with financial basics, the best way to begin saving for college is to pay off all your debt (or at least live within your means and be actively involved in a debt payoff plan). Sound too difficult you say? That sounds like an excuse to me.

Living with debilitating debt and allowing bills to circle your life like a vulture is a surefire way to live paycheck to paycheck and never have the available funds to save for college. What I’m trying to say is this: paying for college isn’t some magical happenstance that you uncover on some random day. It’s going to take hard work, and in some cases, a change in your financial landscape.

Regardless of your current income level, you have the ability to save for your children’s college fund. You might have to trim your expenses, adjust your spending habits, and redirect your lifestyle in order to free up money for the college fund. But if you want to send your kids to college without financing 100% of their education with borrowed money, then you’ll have to decide what’s more important.

Think of it like this; if you can scrounge up even $100 a month to save for your child’s college when they’re born, you’ll end up with $21,600 (and that’s without interest or anything). Sure, that might not pay for 4 years of tuition, room, and board, but it’s definitely a great start.

Saving For College – 529 Plans and Educational Savings Accounts

A 529 Plan is a tax advantaged college savings account designed to encourage families of any income level to save for their children’s education. 529 Plans are “qualified tuition plans” sponsored by states, state agencies, and educational institutions and are authorized by section 529 of the IRS (hence the name 529 Plan).

The encouragement to save for college within a 529 Plan comes in two forms: the ability to save money free from Federal taxes and the ability to receive a deduction on State taxes. One benefit to a 529 Plan is that anyone, upon creation of the account, can be named the account’s beneficiary, regardless of age.

The 529 Plan is a lot like a Roth IRA for your college savings fund. The savings will grow tax-deferred and any withdrawal is tax-free as long as you use the money withdrawn for qualifying educational expenses.

A Coverdell Educational Savings Account (ESA) is another tax advantaged college savings account which is meant to inspire families to save for future educational expenses. The difference between an ESA and a 592 Plan is that an ESA’s beneficiary must be a student under the age of 18.

An ESA also has a maximum annual contribution limit of $2000 and the owner of the account has the freedom to choose what types of securities they would like to invest in (stocks, bonds, ETFs, mutual funds, etc.).

With both types of college savings accounts, you’ll incur a hefty 10% tax if you withdraw any amount of money from either account and use it for non-education related expenses.

Paying For College – Grants and Scholarships

No matter how much or how little you’re able to save for your child’s college education, you’ll always want to be aware of and informed about college grants and scholarships. After all, this is free money we’re talking about.

Scholarships are offered by high schools, colleges, and other organizations usually recognizing some sort of educational, athletic, or humanitarian achievement. Scholarships vary by amount and length. Some are one-time gifts and others are recurring payments made as long as grades and other collegiate performances are maintained.

Information about college scholarships is usually available from your high school, your hometown city hall, and the university you wish to attend. You can also search for scholarships on the web. Some of these scholarships may be smaller than a say a university’s alumni scholarship, but $500 here and $1000 there really starts to add up.

Grants are another “free money” option. The government offers need-based grants to families with a low income. Other organizations are free to offer grants to students that show academic promise or that meet other requirements.

Paying for College – Financial Aid Student Loans

There are numerous kinds of financial aid and student loan programs available, but these loans should be your last resort when it comes to financing college. I’m not saying student loans are bad, but financially responsible parents won’t rely solely on borrowed money to fund their children’s college. As I mentioned earlier, if you save even $100 a month, you can drastically cut the amount of money you need to borrow to send your child to college.

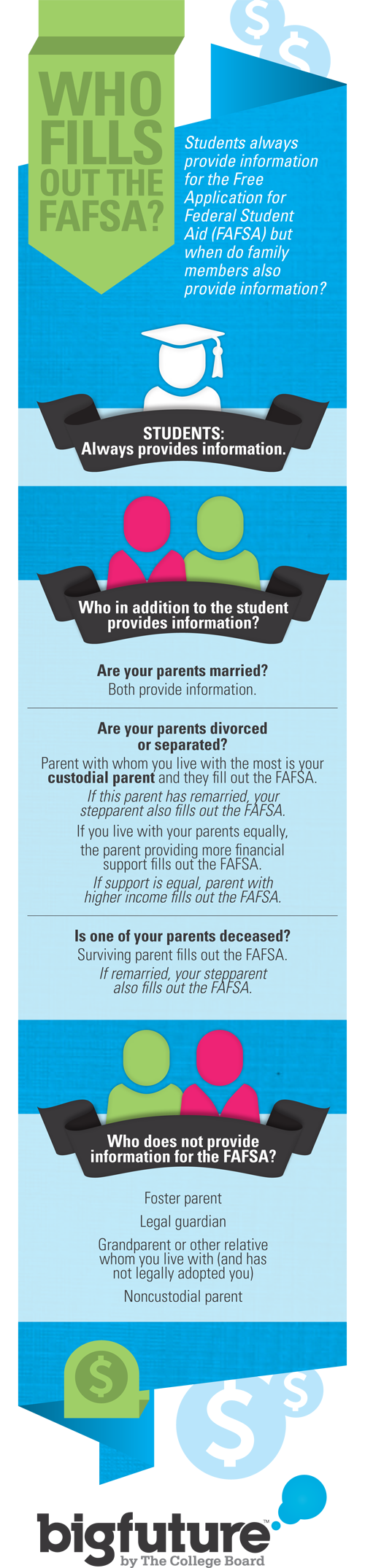

There are Federal Stafford Loans, Perkins Loans, Plus Loans, and numerous other student loans available from private institutions. If you qualify, you can apply for subsidized student loans that are basically interest free until you graduate and begin loan repayment. FAFSA is your Free Application for Federal Student Aid.

Final Comments

Jamie Scott from CreditDonkey also reminds you that while “student credit cards are a convenient option to help students pay for short-term small expenses such as groceries,” there are other options available for long-term larger expenses such as tuition.

The bottom line is that you’ll probably use two or three different sources to fund your child’s college expenses. Don’t give up just because of your low income and don’t think that your high salary will always be there for you. No matter where your income level is at, research, preparation, and responsibility will go a long way when it comes to saving and paying for college.

******

Today’s guest post is from Jamie Scott, social media advocate with CreditDonkey. Jamie helps parents and students prepare for college by evaluating student credit offers. As a parent herself, she knows all too well the concerns most families have about responsible credit usage.

It is estimated that by the time a single child reaches the age of 18, his parents will have spent approximately $300,000, according to the U.S. Department of Agriculture (which releases annual reports on family spending). And that doesn’t include the cost of college. Of course, this report factors in housing, childcare, food, transportation, healthcare, and a number of other elements. But it comes out to about $13,000-14,000+ per year in expenses for a child in a median-income household (earning roughly $60,000-100,000 annually in taxable income). Unfortunately, your costs don’t end when your kids head off to college. In fact, they could increase significantly. You’ll still have to pay for your own home, car, food, and more, but you’ll also be on the hook for additional living expenses for your kids since they are no longer at home, not to mention tuition, books, fees, and other costs associated with college – unless of course you decide not to pay.

It is estimated that by the time a single child reaches the age of 18, his parents will have spent approximately $300,000, according to the U.S. Department of Agriculture (which releases annual reports on family spending). And that doesn’t include the cost of college. Of course, this report factors in housing, childcare, food, transportation, healthcare, and a number of other elements. But it comes out to about $13,000-14,000+ per year in expenses for a child in a median-income household (earning roughly $60,000-100,000 annually in taxable income). Unfortunately, your costs don’t end when your kids head off to college. In fact, they could increase significantly. You’ll still have to pay for your own home, car, food, and more, but you’ll also be on the hook for additional living expenses for your kids since they are no longer at home, not to mention tuition, books, fees, and other costs associated with college – unless of course you decide not to pay.