October 1 is on the horizon and that means the FAFSA will be available for students to complete and file. Believe it or not, many students don’t bother completing it and that’s a decision you and your student might regret.

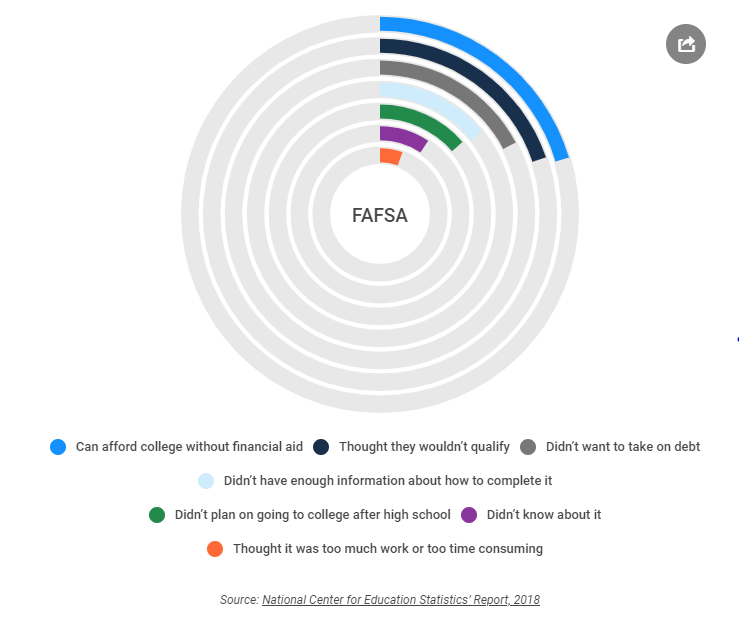

According to the National Center for Education Statistics, Only 65% of high school seniors complete the FAFSA, Why don’t more fill it out? Most either can afford college without financial aid or think they won’t qualify for financial aid. Other reasons include a lack of information — and just planning on skipping college entirely.

Completing the FAFSA is an essential step of the college application.

Why bother completing the FAFSA if you don’t need financial aid?

Even if you and your student can afford to pay for college, why would you pass up free money? Colleges use the FAFSA when distributing merit aid and even some private scholarships require a completed FAFSA.

If you need financial aid, how can completing the FAFSA help?

If you need some form of financial aid to pay for a college education, you MUST complete the FAFSA. In order for students to qualify for federal student loans, state loans, and work-study, they must submit the form. The FAFSA is also required if you plan to take out a Parent PLUS loan to help your student pay for college.

In addition, many students are eligible for federal Pell Grants. High school graduates who didn’t complete a federal financial aid application missed their opportunity for part of $2.6 billion in free money for college, according to NerdWallet’s annual analysis of federal financial aid data.

The money went unclaimed by 661,000 members of the Class of 2018 who were eligible for a federal Pell Grant but didn’t complete the Free Application for Federal Student Aid, or FAFSA.

How much time does it take to complete the FAFSA?

The FAFSA has over 100 questions, which can take anywhere from a half hour to an hour to complete. According to data compiled by Finder.com, new applications less than an hour, averaging 35 minutes. Renewing your application takes even less time — 23 minutes on average. Filling out the FAFSA for the first time takes the longest since you need to fill in answers for each required question.

The bottom line: complete the FAFSA. It doesn’t take that long and most students qualify for some form of financial aid. That doesn’t mean you have to accept it, but why not have that option? And you certainly don’t want to miss out on some of that FREE money!

I

received an email from a concerned parent whose student was going to be

attending orientation next week. In the email, he confessed that he might need

some help with information regarding financing his son’s college education. I was

surprised that he waited so long. Unfortunately, I had to advise him that at

this point his only options were private loans and advise his student to apply

for scholarships over the summer.

Parents should consider college funding even before their student applies to college. The inevitable result of lack of planning is parents and students borrowing to pay and usually borrowing more than they can repay after graduation.

What

do the statistics say?

With

school starting shortly, student loan borrowing often appears in the news. It’s

especially prevalent now with presidential candidates promising to erase

student loan debt. Wherever you stand in the political landscape, it’s clear

from the statistics that students have borrowed more than they can repay.

According

to a 2018 report by the Federal Reserve Bank of New York, as many as 44.7

million Americans have student loan debt, that’s one in five adult

Americans. The total amount of student loan debt is $1.47 trillion as

of the end of 2018 — more than credit cards or auto loans.

How

do you make wise financial choices?

Before applying to college, you and your student should investigate the cost. You can gather the information either on the college website or by using College Navigator. When viewing these figures, you should also research the college’s financial aid statistics—what percentage of students are awarded aid, how much aid is awarded and how much do students typically borrow. Since every family’s financial situation is different, these figures should help determine if the college is affordable to attend.

How

does financial aid play into the equation?

If

you complete the FAFSA, your student will receive some form of financial aid.

The most common is student loans, but colleges also award grants and merit aid

as well. Always complete the FAFSA, even if you don’t think you will qualify

for aid. Colleges use the information on the FAFSA when awarding scholarships

and grants. No FAFSA, no aid.

What’s the key to avoid borrowing too much?

Use repayment calculators before you sign on the dotted line. The rule of thumb is that students should only borrow as much to pay for college as their first year’s salary. By keeping your debt under one year’s salary, you won’t have to put more than about 10% of your income towards student loan payments. Borrowing more than your student can afford to repay sets them up for overwhelming debt after graduation. Your student can look at salary comparisons for their anticipated career at PayScale.com.

How

can you avoid borrowing to pay for college?

The key to not borrowing to pay for college is to receive merit aid, grants, and outside scholarships. Your student should apply to a college at the top of his or her applicant pool. This means the college will be more likely to award aid to attract your student. Grades and standardized test scores are also a key factor in awarding aid. Your student should focus throughout college to pursue excellence in these areas. And, don’t forget outside scholarships. Your student should focus time and effort in applying to every scholarship he or she qualifies for. This means starting early and planning to submit the best application. Click here for scholarship application tips and see how your student can win enough money to pay for college.

Finally, borrow wisely. Only borrow what you need. Your student can borrow the maximum amount, but only borrow what is necessary. Just because you can, doesn’t mean you should. Choose the loans with the lowest interest rates first.

If you’re a parent with a college-bound teen you might be feeling just a bit overwhelmed. With tuition costs rising and many colleges reducing their financial aid packages, it’s easy to wonder if you’ll be able to afford that hefty college price tag and focus on college sticker shock. Whether you are looking at fall college admission payments coming due, or you have several years to go before forking over the cash, you’ll appreciate these simple cost savings tips.

Encourage your teen to search and apply for scholarships. There are all types of scholarships available for all types of students at all ages and education levels. Summer is the perfect time to search and apply, thus conquering summer boredom.

Get college credit early with AP exams. If your teen is enrolled in high school AP courses, make sure they take the AP exams. If they score well, they will receive college credit, which can save you thousands of dollars in tuition alone.

Don’t discount private universities. Your EFC (Expected Family Contribution) will be the same no matter which college your teen attends. Private universities often have substantial alumni donors and also have the largest aid packages with many paying the total cost of tuition.

Consider programs

that provide funds during college in exchange for a service commitment. These

programs such as ROTC, AmeriCorps, VISTA and

the Peace Corps offer tuition reimbursement, stipends and also provide an

opportunity to serve.

Apply for financial

aid even if you don’t think you will qualify. Every family should

complete the FAFSA (Free Application for Federal Student Aid). Every college

uses this form to distribute need-based and non-need based aid. Even if you

don’t qualify for need-based aid, your teen might qualify for an academic

campus-based scholarship.

Be a penny pincher. You

can save big bucks on textbooks, computers, meal plans, dorm furnishings and

transportation. Investigate alternatives to paying top dollar for new items and

save on second-hand items.

Encourage your teen

to take summer classes at your local community college. The

cost for these courses will be substantially less that at a four-year

university. However, make sure that these credits will transfer to your teen’s

chosen college upon completion.

Before your teen heads off to college, create a simple budget that will

help your teen and your family plan for college-related expenditures. These

simple college cost savings tips should help you save a large chunk of change;

and in today’s economy, every dollar counts.

As the costs of college keep rising each year, many students and their families find it necessary to rely on financial aid to help pay for college. There are many different types of financial aid available, and knowing which one best matches your situation is key to not only choosing the right type of aid, but also maximizing the amount that you can qualify for—and minimizing your debt obligations later on.

Financial aid is a critical part of the college application and attendance process. It can make college a reality for many students and help bridge the gap between family contributions and the overall cost of attendance. Some types of aid don’t need to be paid back; others can leave you in debt for years to come.

With that in mind, it’s important to understand how to best approach the financial aid process, and how to set yourself up for financial success later by putting thought into the process now.

What Should You Start With?

The first step in the financial aid process should be completing the FAFSA. Short for the Free Application for Federal Student Aid, the FAFSA walks you through a complete picture of your finances. If you’re a dependent student—most first-year students are—then it also includes questions about your parents’ financial situation and their potential ability to assist in funding your education.

The federal government is the biggest source of financial aid for college students, and before it’ll consider you as eligible for aid, you’ll need to complete the FAFSA, which serves as your application for all federal aid. The FAFSA is completed online, it’s free, and there is plenty of help available to assist you and your family in filling it out.

What’s the Takeaway from the FAFSA?

Once your FAFSA is submitted to the federal government along with your choices of colleges, a Student Aid Report, or SAR, is generated from the information you entered. The SAR explains how much your expected family contribution (EFC) is. The government takes the position that it’s your responsibility to pay as much as you can to your own education first; the EFC is how much the Department of Education thinks you and your family should be able to contribute to the total cost.

Each year, colleges publish an amount called the cost of attendance. It includes all the expenses that go into attending that school: tuition, room and board, textbooks, fees, and other things like living expenses throughout the school year. Your EFC is subtracted from the Cost of Attendance, and the resulting balance is considered your financial need. The federal government sends your SAR to the schools you listed, and they compile a financial aid package to offer you.

Your federal financial aid package could include a variety of aid products including Pell grants, unsubsidized and subsidized federal student loans, and more. You should always consider Pell grants and subsidized federal aid first. A Pell Grant is a type of aid that does not require repayment, and subsidized loans do not accrue interest while you’re attending school.

After looking at your offer, you may find that your financial aid package isn’t enough to cover the entire bill, but there are other options to consider such as scholarships.

Should You Consider Scholarships?

The short answer is “YES, absolutely!” Scholarships, like grants, are essentially free money that you don’t have to pay back. They should always be a consideration regardless of what year you are in college. You can apply for new ones every year, and there are tons of sources to find scholarships. They can really make up the difference up between the cost of attendance and your financial aid package. Start early and often. If the FAFSA wasn’t so important, this would be the first place to start.

There are thousands of scholarships available every year, but they’re highly competitive. Each program has its own application criteria and deadlines, and the best way to maximize your chances of winning one is to ensure that you follow the program’s directions and meet all of the deadlines—preferably applying as early as possible. The best way to go about winning scholarships is to just keep on applying to any legitimate opportunity you can find.

Is There a Last Resort?

If you find there’s a funding gap left over after scholarships, grants, and other federal aid, then you still have one option: a private student loan. There are distinct differences compared to federal student loans do, but sometimes they’re a necessary tool to cover that funding gap.

Offered by banks, credit unions, and other lenders, private student loans are based upon your creditworthiness; as a result, most students find that they need a qualified cosigner for approval. Further, you may find even the best private student loans still have high interest rates compared to federal loans. After all, interest rates are generally higher for private loans. Also, they don’t come with a grace period like a federal loan. That means you’ll need to start paying it back immediately, just like a car loan or mortgage, even if you’re still in school.

It is clear that private student loans are not as desirable compared to their federal counterparts; however, sometimes they’re a viable option if it’s crunch time.

The thought that crosses every students mind is the dreaded debt they will inevitably find themselves in years and years down the line. It seems that students are now facing an uphill battle when it comes to their student loan debt. You will struggle to get a credible job without the relevant qualifications, which means at some point you’re going to need to go and study at college. Unfortunately, college fees do not come cheap. Many people have to boycott college altogether because they simply can’t afford it. It’s such a shame that many youngsters have to miss out on getting the best education because money is short. If you are lucky enough to get into your chosen subject of education, here are a few pointers which will help you to avoid the dreaded debt.

Social Butterfly Without the Burden

You’ve gotten into the college of your dreams and you can’t wait to make new friends and memories, but you’re a little worried about your budget. You are not alone. Every single person is worried. Socializing at college doesn’t have to be super expensive. There are several ways in which you can save money and still have a great time. Join loyalty schemes and get to know which bars and restaurant your campus is associated with. The chances are you will be able to get discounts all year round, which means cheap drinks and food whenever you and your friends go out. Change up how you socialize with your friends too. Spend more time around people’s places instead of going out and hold movie nights instead of taking a trip out to see the latest blockbuster.

Room and Board Can Cost A Little

Room and board costs can stump a lot of students. Seriously, how can it cost so much to live in a pitiful little room with no bathroom? If you haven’t already thought about it, maybe you could consider online education to save yourself a lot of money. Partaking in an online bsw, for example, would allow you to stay at home and would cut your student debt almost completely. By opting to be educated virtually you wouldn’t be overburdened with outrageous costs, but keep in mind you need to be super motivated in order to get a degree from an online format.

Save, Save, Save

Before your further education suddenly hits you like a brick wall you should consider saving up some cash so you have got a head start. The summer before you’re due to head off to college you should definitely consider getting a job. It will not only give you a boost to buy all of the things you’ll need when you’re first moving away, but it will also motivate you to earn some money whilst you’re getting your education. Many students find it useful to take on a part-time job whilst they’re studying. It will ease the burden much more in the future.

So take these points into consideration if you’re due to start your higher education. Maybe you have a younger sibling who is ready to go to college and you want them to learn from your mistakes. Let’s start imparting our wisdom on others and stop the vicious cycle of student debt!

How can you assure that your student receives an affordable college education?

I received this comment on one of my blog posts from a parent:

I am so unprepared. I had no idea about the steps I should have taken. My daughter officially started class yesterday and I am struggling to figure out how to pay for it. She made above average grades and a wonderful ACT so I really figured she would get some kind of offer. She did not and we are middle class but FASFA says we make too much money. I am in such need of help and guidance.

This is the predicament of so many middle class families. Their student applies to college, is accepted, and receives no financial aid. They are stuck with the dilemma of sending them to this college and finding a way to pay, or disappointing their child and also incurring debt so she can attend.

Before you find yourself in this situation, here’s my advice on how to get an affordable college education and avoid this difficult conversation with your student.

Step 1—Get good grades in high school

There is nothing more important to receiving good financial aid than good grades. These habits actually begin in middle school and build until your student applies to colleges. Good grades represent a commitment to education and academic excellence—two things colleges look for in an applicant.

Step 2—Take AP Honors and/or Dual Credit classes

Colleges look for students who take these college-level courses increasing your student’s chances of merit aid. But the best benefit of these classes is the cost savings you will realize. If your student takes AP classes, takes the test and does well, he will receive college credit. Dual credit courses are taken during high school and once completed, count for college credit. Comparing the cost of an AP test or Dual Credit course to the cost of a course in college, you save thousands.

Step 3—Score well on the PSAT

If your student scores well on the PSAT and is a National Merit finalist, the financial flood gates from colleges will open. Your student should take this test as seriously as she does the SAT or ACT. It’s more than a practice test!

Step 4—Score well on the SAT and/or ACT

Standardized test scores will have an effect on the college’s financial aid award. Good grades, a good essay, and good test scores will make you a desirable candidate for admission which can mean merit aid.

Step 5—Apply for scholarships like it’s your job

Your student’s #1 job in high school is to apply for scholarships. Don’t wait until senior year. There are scholarships available for all ages. The more he applies, the better his chances to win. Keep applying during college too!

Step 6—Apply to the right college

If your student is at the top of the applicant pool, it is more likely she will receive financial aid. Colleges reserve merit aid for the students they want to attract. Applying to an elite college where there are hundreds of applicants with better grades and test scores the chances of being awarded financial aid are slim. But if your student applies to a college where most of the applicants scores and grades are average and your student’s are stellar, the chances of receiving financial aid are good.

Step 7—Search for colleges with good financial aid footprints

Use sites like CollegeNavigator and CollegeData to find colleges that award a high percentage of financial aid to admitted students. If your student applies to a college that offers a low percentage of aid, you are gambling with your financial aid. A sure bet would be a college that meets a high percentage of a student’s financial need.

Step 8—Compare financial aid awards and appeal

Once your student receives financial aid awards compare them with one another. Use the top awards to bargain with the college your student most wants to attend. Appeal the awards and ask for more aid. If you don’t ask, you won’t receive. Colleges have award money available from those students who declined admission. If they really want your student, they might increase the award.

Step 9—Work during high school and college

You would be surprised at how much money your student can earn during high school. If he or she is too young to work at traditional jobs, there is always babysitting and yard work. Be sure you put the money in your own account, however. Student savings will decrease your EFC substantially. And during college, your student should work. Studies show that students who work are often better students and time managers.

Step 10—Go for the gold

If your student is open to attending a tuition-free college your worries will be gone! These colleges are not for everyone but they are worth investigating: 8 Colleges Where Students Attend for Free.

Best advice: Determine before your student applies to college how much you can afford to pay if he or she doesn’t qualify for financial aid. Even if you follow all of these steps, be prepared for this possible outcome. If you do, you and your student won’t go into debt or be disappointed when the answer is no.

Last night I spoke with a relative whose son just had a baby. The parents were already developing a strategy for paying for college. When she told me they were planning to enter their child in beauty pageants to foot the bill, I had to interject. I told her this was certainly going to cost the parents money and the rewards would probably not be worth the effort. Then I told her the best strategy to pay for college: good grades.

According to an NACAC survey, colleges rank the grades in college prep courses, the strength of curriculum, and grades in all courses as the top factors in the admissions decision. But here’s the added bonus, those grades can also net a student huge rewards in financial aid. Many colleges will award automatic full-ride scholarships to students with high GPAs and class rank.

Instead of placing all your college money “eggs in one basket”, in addition to saving, use these three strategies to create a plan that will pay the college tuition bill:

Focus on academics

The tone is set freshman year. Make it a goal to choose the pre-college courses (AP and Honors) and get the best grades possible in these courses. If your student does poorly freshman year, it makes it difficult to catch up later. All throughout high school, your student should place high value on academic progress: commit to study, prepare for class and tests, seek help when needed, and put academics before any other activity.

Apply for outside scholarships

Start applying for scholarships as early as possible. Waiting until senior year is a poor decision. There are scholarships available for all ages. It should be your student’s “job” during high school to search and apply for scholarships. An hour a day can produce huge rewards and start racking up funds each year to make a huge dent in the tuition bill.

Chose the colleges with the best financial aid footprint

What does this mean? Look for colleges with a high percentage of financial aid. Every college reports the statistics related to their financial aid profile. These statistics can tell you how generous they are with their scholarships and grants and also the percentage of students who receive help with their tuition.

The best resource available for these statistics is College Navigator. You can enter the name of the college, or search using criteria such as location, size, and degree plans. Once you’ve pulled up the data, you can use it to compare colleges.

If you use these three “paying for college” strategies, no matter where you are in the process, your student should be able to graduate from college with little or no debt. Additionally, you should be able to pay for college without borrowing or dipping into your retirement (which I never recommend).

Paying for college is an uphill battle filled with mindboggling FAFSA paperwork and a steady stream of education bills. Stress due to how individuals will pay for college, housing, textbooks, and extra fees can be a continual buzz at the back of the mind. In order to avoid thousands upon thousands of dollars in student loans, college students and their families can strategically make financial and professional decisions that will maximize the amount of federal and company student aid they will receive.

Employer-Provided Educational Assistance

Students, prospective students, and parents can decrease the out of pocket cost of college by pursuing a job at a company that has educational assistance or scholarship programs. Many smaller companies have a long history of providing scholarships for their employees and their employee’s children.

On April sixth of this year, Starbucks led the employer educational program charge by offering to pay for the tuition for all part and full-time employees. Employees can choose any one of the 49 undergraduate programs at Arizona State University online program. Beyond Starbucks, there are dozens of employers who have educational benefits programs. The majority of the programs offer anywhere from $1,000 to $5,250 in educational aid per year.

Students should also look into deducting their education from their taxes as a work-related fringe benefit. Educational fringe benefits help professionals seek the education required when they meet one of the following requirements:

They are required to receive the education by their employer or the law to keep their salary, status, or job.

The education will help improve or maintain a skills needed for your job.

They also cannot:

Allow you the possibility of entering a new field.

Allow you to receive minimum educational requirements for your field.

Does it sound like you might qualify? What individuals can deduct is just as expensive. You can dive further into the topic here.

Extended Family Contributions

Your grandma or grandpa planning on helping you pay for college? Before they write you a check, you can strategize how and when the grandparents help you pay for college to minimize what they pay in taxes and maximize how much financial aid you receive.

First off, grandparents can maximize the financial benefits of aiding their grandchildren by sending the tuition money directly to the college. Paying the tuition directly qualifies the educational contribution as a gift tax exclusion. What does this mean? The grandparents will not need to report the contribution to the IRS.

It should be noted that only tuition is considered a gift tax exclusion. If family members want to help students with other educational expenses, the money qualifies as a gift tax expense. The family member should tally the amount given to the student. If the amount is less than $14,000, the amount given does not need to be reported. Anything over the $14,000 must be reported by the individual who gave the gift. No taxes will need to be paid on the gift until the individual has given more than $5.34 million.

Don’t rush off to tell your grandparents the good news yet. Here’s the bad news: If they help you pay for college this year, it will decrease the amount you will receive in financial aid next year. Unfortunately the people at FAFSA assume if they help you this year, they’ll continue to offer the same amount of aid the following year. You can prevent this fatal mistake by advising your grandma or grandpa to wait until the last year or two of college before helping out.

Paying for college can be expensive, but it can be manageable by developing a game plan. Business educational assistance and familial educational gifts utilized at the right time can be the beginning to a successful financial strategy to pay for college.

____________________________________

Today’s guest blogger, Samantha Stauf, was a first generation college student. Since Samantha graduated two years ago, she’s spent her free time writing articles meant to help current students succeed. You can find her on Twitter at the hashtag @samstauf.

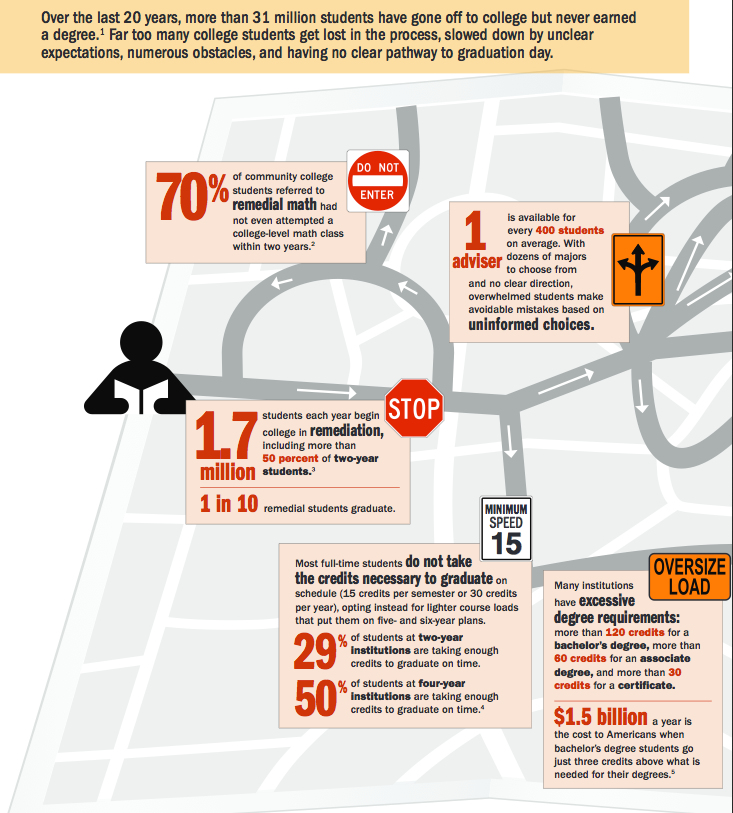

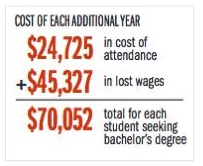

Did you know that at most public universities, only 19 percent of full-time students earn a bachelor’s degree in four years? Even at state flagship universities — selective, research-intensive institutions — only 36 percent of full-time students complete their bachelor’s degree on time.

Nationwide, only 50 of more than 580 public four-year institutions graduate a majority of their full-time students on time. Some of the causes of slow student progress are inability to register for required courses, credits lost in transfer and remediation sequences that do not work. Studying abroad can also contribute to added time and credits lost when abroad. According to a recent report from CompleteCollege.org some students take too few credits per semester to finish on time. The problem is even worse at community colleges, where 5 percent of full-time students earned an associate degree within two years, and 15.9 percent earned a one- to two-year certificate on time.

What is lost when a student doesn’t graduate in 4 years?

MONEY! My good friend, and college counselor, Paul Hemphill of Planning for College put it into perspective recently. (See chart to the right). It’s not just the cost of the education that your student loses, but the earning potential over the additional year or years. Nothing speaks louder than cold, hard numbers.

What can parents do to ensure on-time graduation?

It’s not a difficult task, although the numbers might speak otherwise. Taking control of the process and making a plan will go a long way in ensuring on-time graduation

Show your student the numbers—Nothing speaks louder than showing your student a loss of thousands of dollars in earning potential if they don’t graduate on time.

Help them plan their major and degree plan, ensuring it can be done in 4 years—Help them plan, ask questions of their advisors, and have solid discussions about their career and/or major.

Encourage AP testing and dual-credit courses—With AP testing and dual-credit courses, a student can enter college with multiple credits out of the way. The cost of these tests and courses pales in comparison to the cost of a college credit and extra money paid if they don’t graduate on time. It’s conceivable that with the right planning, a student can graduate in less than 4 years.

Attend community college for the basics during the summer before college—Not only will your student get some courses out of the way at a cheaper rate, they will enter college with credits under their belt.

Use some tough love—Explain the importance of graduating on time and explain that you will support them for 4 years only. After that, the cost is on them. Nothing motivates a teen more than realizing they will have to pay for college themselves.

Below is a neat little graphic (courtesy of Paul Hemphill) breaking it down for you.

Every day parents complain about the high cost of college and the fact that even though they have saved, it’s not going to be enough to cover present day costs. When the kids enter high school, most parents begin to panic. The time has slipped away from them and they are faced with some difficult decisions. The thought of disappointing their kids seems unfathomable and the thought of telling their family and friends that they can’t afford to send their kids to college is even worse.

Consequently, we exhibit behavior that has devastating consequences for us and for our kids:

We make unwise decisions related to student loans

We neglect to tell our kids “no” when a college is beyond our ability to pay

We don’t include our kids in the financial aspects of the decision in the beginning

I read a post by Lynn O’Shaughnessy on The College Solution blog entitled “We are Done Paying for College”— it made me stop and think: what are our priorities as parents? Lynn and her husband began planning when their kids were little. They scrimped and saved and prepared for the day when they would go to college. It required sacrifice and commitment. But they did it and can say that their kids graduated without any student loan debt. You owe it to yourself to read her post, even if your kids are already in high school. It’s a definite wakeup call for all parents of college-bound teens.

Step back and evaluate

What are your priorities? Is college important enough for you to make some sacrifices? This means financial sacrifices and sacrifices of your time.

Make a plan and stick to it

If paying for college means driving an older model car for a few years, do it. If you need to supplement your education savings by taking on a second job and insisting your kids work during high school, make it work. If your family has to forgo some vacations, a new home, or a eating out often, it’s worth the sacrifice. But whatever you decide, make a plan and stick to it.

Be creative and think outside the box

There are so many creative ways to attain a college degree. Your kid isn’t bound to the typical four-year University or attending four consecutive years in a row. It’s also not necessarily essential that they attend college right out of high school. Do whatever it takes to attain the degree without debt and causing the family financial hardship.

It doesn’t matter where you are in the college prep process. You should evaluate your priorities and ask yourself some tough questions. It may sting in the beginning but once you’ve examined your options, you’ll sleep easier and so will your kids.

What is lost when a student doesn’t graduate in 4 years?

What is lost when a student doesn’t graduate in 4 years?